What Is the Best Value Property in Canada? A Buyer's Guide to Finding the Right Home

- Apr 6

- 8 min read

Everyone wants the best value when buying a home. It sounds straightforward, but the answer looks different for every buyer. But here’s the thing: nobody can tell you what the right property is for you. Not an agent. Not a market analyst. Not a headline. The answer isn’t a number on a listing sheet. It’s personal. A property that’s an exceptional deal for one buyer might be a costly mistake for another — even if they’re standing in the exact same living room, looking at the exact same price tag. Before you spend a single hour scrolling MLS® listings or attending open houses, there’s a more important exercise to do. You need to get honest with yourself about the life you’re building.

These are the questions that actually matter.

How to Find the Best Value Property in Canada: Start With Your Life

Most buyers — especially first-time home buyers in Canada — approach the search backwards. They start with listings, filter by price, and then try to make a property fit their life. The questions below flip that process. They’re the questions to ask before buying a house in Canada, and they’re worth answering before you open a search portal — because once you can answer them honestly, you’ll know exactly what you’re looking for and why.

Question 1: How Long Do You Plan to Stay?

This might be the single most important variable in the entire equation, and most buyers either underestimate it or avoid thinking about it altogether.

How long you plan to stay changes what value looks like:

Under 3 years: Transaction costs can add up quickly — and that’s before factoring in mortgage penalties. In Canada, breaking a closed fixed-rate mortgage typically costs the greater of three months’ interest or the interest rate differential; variable-rate mortgages usually carry a three-months’ interest penalty. Add land transfer taxes (which vary by province and municipality), legal fees, and realtor commissions on the sell side, and buying a home you plan to leave quickly could cost you more than renting in some scenarios, even if prices stay flat. The exact hit depends on your province, mortgage type, and purchase price, so it’s worth modelling your specific numbers before committing.

3–7 years: You need to think carefully about resale appeal. Does this property have broad market appeal, or is it a niche home that might be harder to move? Unique can be wonderful to live in; unique can be a liability when you’re trying to sell.

10+ years: You have the time to weather market cycles. You can prioritise what genuinely works for your life over what maximises resale metrics.

Ask yourself: If your life changed dramatically in three years — a new job, a relationship shift, a growing family — would this property work, or would you be trapped?

Your honest answer to that question shapes everything that follows.

Question 2: What Does Your Career Look Like — And Where?

The pandemic reshuffled what proximity to work means for millions of Canadians. But it also introduced a new kind of uncertainty: nobody is quite sure which work arrangements will stick.

Before you commit to a location, think honestly about:

Remote work stability: Is your current remote or hybrid arrangement a permanent policy, or could it change? If you buy 45 minutes from your office assuming you’ll only go in twice a week, what happens if that changes to five?

Career mobility: Are you in a field where your next opportunity might require relocating? A strong national job market in your field is very different from one concentrated in two or three cities.

One car or two? This is a practical question with real financial implications. A home that is cheaper upfront can cost more over time if it requires two cars, longer commutes, and higher transportation costs.

Commute quality vs. commute length: Forty minutes by transit where you can read, decompress, or work is a different experience than forty minutes in stop-and-go traffic. Both matter to your quality of life, and quality of life is the point.

Question 3: What Kind of Life Do You Actually Want to Live?

This question sounds obvious, but most buyers skip it entirely — or answer it based on what they think they should want rather than what they actually want.

Do you want quiet, or do you want energy?

There’s nothing wrong with wanting a calm street where you hear birds in the morning and the loudest thing on a Saturday is your neighbour’s lawnmower. There’s also nothing wrong with wanting to walk out your front door to a coffee shop, a market, and a transit line. Each comes with a very different property profile and, in most Canadian cities, a very different price point. The mistake is buying the quiet suburban home because it seems like the “responsible adult” choice when what you actually want is urban energy, or vice versa, buying the trendy downtown condo because it felt exciting in your twenties when what you actually crave is space, nature, and silence.

Think about your actual weekend. Not your aspirational weekend — your actual one. Where do you spend your time? What do you need nearby to feel like yourself? Buy for the life you live, not the life you imagine you might someday live.

Question 4: Will Your Family Grow — And Do You Want Your Home to Grow With You?

This is a deeply personal question, and we’re not going to pretend there’s a clean answer. But it’s one worth sitting with.

If you’re planning to expand your family, the calculus looks different:

Will you need more bedrooms in 3–5 years? If yes, does it make more sense to buy slightly bigger now, or buy the smaller place and move when the time comes? (See Question 1; your timeline matters here.)

Is the neighbourhood kid-friendly? Proximity to parks, schools, and other families matters in a way it genuinely didn’t before children.

Is there room to adapt? Some properties have the bones to grow with you — a basement suite that could become a teenager’s domain, a garage that could convert to a studio, a large lot that allows for future development. Others are fixed. Know which you’re buying.

If family growth isn’t part of your plan, don’t buy for a family you might not have. Buying a 4-bedroom house because “you never know” means paying for space — in purchase price, property tax, heating, maintenance — that you may never use.

Question 5: Is Real Estate Your Investment Strategy — Or Just Part of It?

This question divides buyers more than almost any other, and it’s one the real estate industry often avoids.

In Canada, homeownership has been enormously wealth-building for millions of people over the past two decades. That’s real, and it’s part of why buying is still a reasonable decision for many Canadians in many markets. But it’s worth being clear-eyed about what you’re actually doing. If you’re putting everything into a down payment and stretching to the top of your budget, you’re making a concentrated, leveraged bet on a single asset. That’s not inherently wrong — but it should be a conscious choice, not a default.

Ask yourself:

What are you giving up? Capital that goes into a down payment isn’t available for a business, an investment portfolio, or an emergency fund. What opportunities or safety nets are you foregoing?

Do you want the optionality of liquidity? Real estate is illiquid. You can’t sell 10% of your condo when you need $40,000 quickly. Some people are completely comfortable with that tradeoff. Others aren’t — and only realise it once they’re in.

Would buying a less expensive property leave you in a stronger financial position overall? In markets where inventory is elevated and negotiating power leans toward buyers, buying at 80% of what you qualify for and keeping capital for other goals may serve your long-term financial health better than maximising what you spend.

There’s no universally correct answer. But “spend as much as the bank will give you” is a mortgage broker’s answer, not necessarily yours.

Question 6: What Do You Want Your Life to Look Like in 10 Years?

This is the question that ties everything together — and the hardest one to answer honestly, because life is genuinely unpredictable.

But the exercise is still worth doing. Not to perfectly forecast the future, but to identify your values and priorities so clearly that you’ll be able to recognise the right property when you see it — instead of rationalising the wrong one.

Try this: picture a normal day in your life ten years from now. Where do you wake up? What’s outside your window? How do you get to work — or do you work from home? Who’s at the breakfast table? What does the weekend look like?

Now work backwards. Does the kind of property you’re currently considering fit that picture? If it does, that’s a strong signal. If you’re finding yourself rationalising why it might eventually work, that’s worth paying attention to.

This isn’t abstract philosophy. It’s the most practical thing you can do before entering one of the biggest financial decisions of your life.

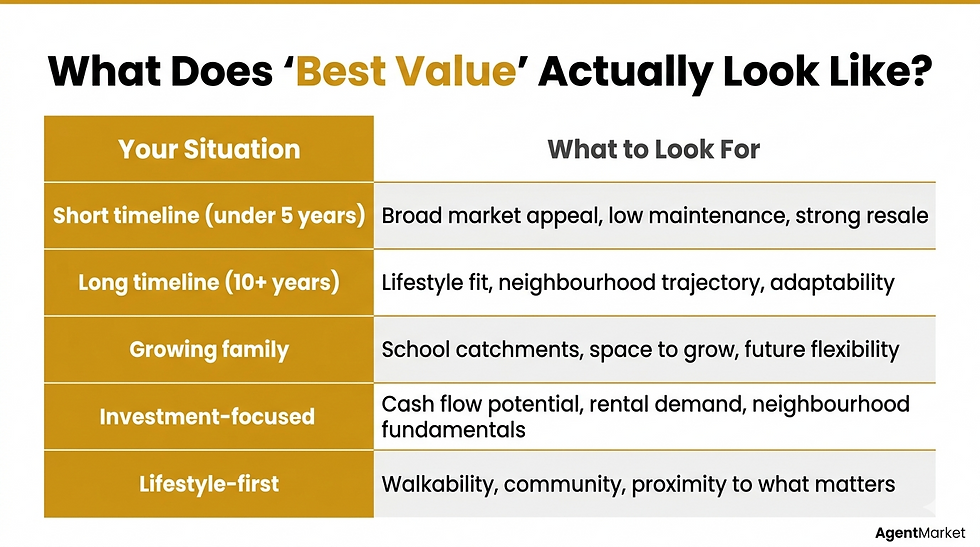

Putting It Together: Your Personal “Best Value” Framework

Once you’ve worked through these questions honestly, market data becomes much more useful. A neighbourhood that’s “up and coming” is interesting if you’re buying for 10 years, but largely irrelevant if you’re planning to move in three. A two-bedroom condo can be excellent value if your life is right-sized for it, and a frustrating constraint if you’ll outgrow it within 18 months.

Here’s a simple way to frame it:

These aren’t mutually exclusive. But knowing which one or two factors are most important to you makes the decision exponentially clearer.

Frequently Asked Questions

What does “best value” mean in real estate?

It depends on your goals. For a long-term owner, best value might mean the home fits your life, even if it isn’t the cheapest option. For someone buying for five years, it likely means broad market appeal and low maintenance. There’s no single definition — which is why the right starting point is your life, not the market.

How do I find the best value home in Canada?

Start by defining your timeline, lifestyle priorities, and financial philosophy. Once you’re clear on those, you can evaluate properties against your actual criteria rather than reacting to listing prices. The right agent can help you spot where genuine value lies in your specific market.

What are the real costs of buying a house in Canada?

Typical closing costs include land transfer tax, legal fees, title insurance, and home inspection costs — plus potential mortgage penalties if you’re breaking an existing mortgage. The total varies by province, mortgage type, and purchase price, so model your specific numbers before finalising your budget.

Is it better to buy now or wait?

That depends on your personal timeline and financial readiness more than market timing. A market that favours buyers today may look different in 12 months. The more useful question is whether you are ready — not whether conditions are perfect.

Your Quick-Reference Checklist

Whether you’re a first-time buyer or returning to the market after years away, here are six questions to ask before buying a house in Canada:

How long do I realistically plan to stay in this property?

Is my career stable, and does it tie me to a specific location?

What does my actual day-to-day life look like, and what does my home need to support it?

Is my family likely to grow, and do I need the home to accommodate that?

Am I keeping capital for other financial goals, or putting everything into this purchase?

Does this property fit the life I want to be living in 10 years?

If you can answer all six with clarity, you’re ready to start comparing properties with purpose.

One More Thing: The Right Agent Makes This Easier

Once you’ve done this thinking, the conversation you have with a real estate agent becomes completely different. Instead of “show me what’s available in my budget,” you’re walking in with a clear picture of your timeline, your lifestyle needs, your financial philosophy, and your long-term vision.

A good agent will use that to your advantage — helping you identify which properties actually fit, what to look past, and where real value is strongest in your local market. The challenge is finding an agent who listens first and sells second.

If you’re not sure where to start, AgentMarket.ca lets you compare agents side-by-side, review their credentials and approach, and request personalised proposals — all before sharing any contact information. It’s a useful way to find someone whose style matches how you want to make this decision.

The information in this article is intended for general educational purposes and does not constitute financial or legal advice. Real estate markets vary significantly by region. Always consult qualified professionals before making property decisions.